Just days before the tiny nation of Gibraltar was said to draft their first initial coin offering (ICO) regulations, Financial Market Supervisory Authority (FINMA) of Switzerland appears to have stolen its thunder in an eleven page document published today. It could be the standard by which developed countries look to install their own versions.

Also read: Citibank India Bans Bitcoin

Switzerland Publishes ICO Guidelines

“The guidelines also define the information FINMA requires to deal with such enquiries and the principles upon which it will base its responses,” an agency press release began, “creating clarity for market participants.”

ICOs have bedeviled regulators the globe over since their inception Summer of 2013 as a creative way to crowdfund projects. They deliberately mirror initial public offerings, IPOs, which are famously used to bring traditional companies to market. However, IPOs have taken all the trappings that come with success: barriers to entry making them a very expensive proposition, requiring gaggles of lawyers and regulatory hoop-jumping. ICOs, due to their nascency, have gotten around all that to the tune of 6 billion USD in 2017 alone.

“FINMA has seen a sharp increase in the number of initial coin offerings (ICOs) planned or executed in Switzerland and a corresponding increase in the number of enquiries about the applicability of regulation,” the regulator insists. Following up on their Spring of last year Guidance document, “setting out how it intends to treat enquiries from ICO organisers,” FINMA wishes to solidify “transparency at this time” as it “is important given the dynamic market and the high level of demand.”

ICOs are a participatory token economy in the literal, digital sense. They usually focus upon a specific project, and combinations and permutations on this idea are as vast as the myriad of ICOs themselves: ownership in a company, payouts, tradeable coins, some of which are expected to appreciate beyond just being a digital stock certificate. They’re an adventuresome investment, and, as these pages have well-documented, slickly written white papers and website landing pages have often amounted to little more than exit scams.

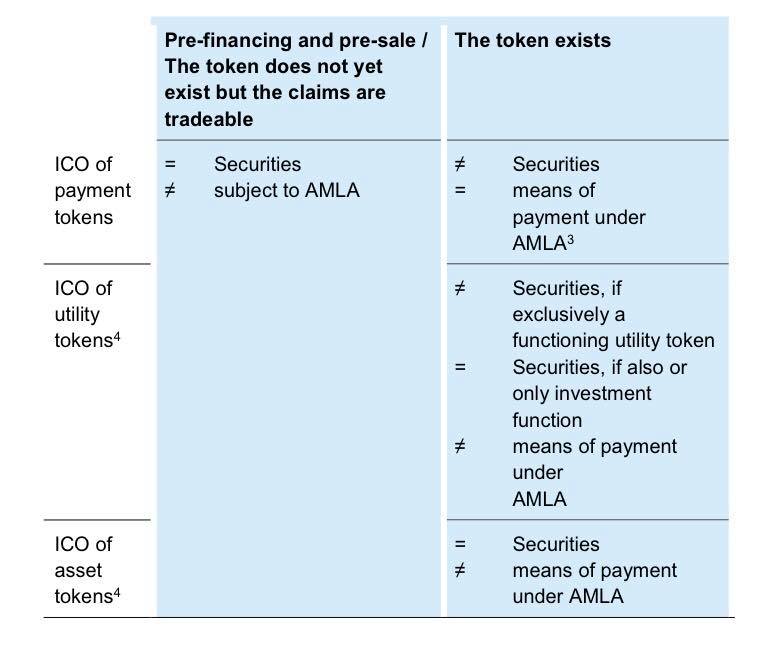

Not All ICOs are Equal

A vast majority of ICOs rely upon the Ethereum platform and its Ethereum Request for Comments (ERC20), which is used for smart contracts. Something like over twenty one thousand such contracts exist, and estimates hold that ERC20 commands a supermajority ICO marketshare.

Swiss guidelines are “not applicable to all ICOs. Depending on the manner in which ICOs are designed, they may not in all cases be subject to regulatory requirements. Circumstances must be considered on a case-by-case basis […] At present, there is no ICO-specific regulation, nor is there relevant case law or consistent legal doctrine.” As such, “FINMA will focus on the economic function and purpose of the tokens (i.e. the blockchain-based units) issued by the ICO organiser. The key factors are the underlying purpose of the tokens and whether they are already tradeable or transferable.”

Swiss guidelines subdivide tokens into three classes: payment, utility, and asset. Payment tokens are basically cryptocurrencies as most understand them; utility tokens are access to services; asset tokens function more like derivatives, bonds, equities, and can serve as interest or dividend payments.

FINMA’s deepest worry involves anti-money laundering (AML) law subversion. “FINMA’s analysis indicates that money laundering and securities regulation are the most relevant to ICOs,” and as such guidelines contain “requirements for financial intermediaries including, for example, the need to establish the identity of beneficial owners.” Revealingly, the agency baldly asserts, “Money laundering risks are especially high in a decentralised blockchain-based system, in which assets can be transferred anonymously and without any regulated intermediaries.”

Supportive of Blockchain Technology

ICOs with payment token arrangements FINMA won’t be thought of as securities, and instead be required to comply with AML regulations already in place. Additionally, utility token ICOs “do not qualify as securities only if their sole purpose is to confer digital access rights to an application or service and if the utility token can already be used in this way at the point of issue.”

Asset token ICOs, however, “FINMA regards asset tokens as securities, which means that there are securities law requirements for trading in such tokens, as well as civil law requirements.” Where there are hybrids, it appears the most regulation applies rather than a default to a less regulated token.

The Swiss body was careful to suggest it supports blockchain development, and it quotes FINMA head Mark Branson as insisting, “The application of blockchain technology has innovative potential within and far beyond the financial markets. However, blockchain-based projects conducted analogously to regulated activities cannot simply circumvent the tried and tested regulatory framework. Our balanced approach to handling ICO projects and enquiries allows legitimate innovators to navigate the regulatory landscape and so launch their projects in a way consistent with our laws protecting investors and the integrity of the financial system.”

Do you think FINMA’s guidelines will be the world standard? Let us know in the comments section.

Images courtesy of Pixabay, FINMA

Need to calculate your bitcoin holdings? Check our tools section.

The post Switzerland Enacts ICO Guidelines appeared first on Bitcoin News.

Bitcoin.com is author of this content, TheBitcoinNews.com is is not responsible for the content of external sites.

Our Social Networks: Facebook Instagram Pinterest Reddit Telegram Twitter Youtube