SWELLENDAM – The parody I scripted about a year ago, pitching Darth Vader representing cryptocurrencies against Blackbeard the Pirate representing gold, with both jostling for position as a viable option to fiat currencies, may have become less sardonic.

The price of one Bitcoin has overtaken the price of an ounce of gold for the first time – touching on $1 300, with gold at about $1 240 on the day. Since then, both have eased, swapping lead positions in a market dance, but with gold being distinctly outpaced. Of course, one can make too much of it. Each market has its own peculiarities and driving forces.

Cryptocurrencies in particular are still in a very volatile stage. Bitcoin rose to record levels on speculation around a Bitcoin ETF, and falling nearly $300 on the application being turned down; but bouncing back remarkably to about $1 250 this week. Bitcoin.com points to other supporting factors in “Increased regulation from Chinese authorities, demonetisation in India, recently passed legislation in Japan, as well as the general instability of fiat currencies”. Analysts share a wide range of future price predictions. Gold on the other hand, has its own woes with US interest rates, a dance partner it prefers over cryptocurrencies and depressing the price to below the $1 200 resistance level this week.

The bitcoin/gold paring may deserve more coverage than it has been given in the financial media because of what they have in common – a shelter for flight from our current troubled means of exchange. The picture that I painted of the past and the future doing a dance on the corpse of the present is not as abstract and futuristic as it may first appear. That context deserves repeating.

We now have three potential forms of money, each with their own element of fiction. If you strip gold of its ancient allure, its historic backing of paper currencies and its investment and adornment image, you could certainly posit the Keynes view that it is a “barbarous relic”. If you interrogate bitcoin’s mysterious and anonymous founding, creation structure and block chain security, you could equally have some qualms. But both do not come near the degree of fiction that permeates fiat currencies. Debt is a fiction. It is nothing more than a promise to pay sometime in an ever-delayed future – a very empty promise considering the increasing extent to which the gap between debt creation and the means to pay is beyond redemption.

In stating the case for cryptocurrencies, Bitcoin.com quotes Adam Davies, a consultant at Altus Consulting, as saying: “People are unsure about what is going on in the world, and digital currencies unlike the UK pound sterling have been hit badly because of Brexit, so people are looking to divest into bitcoin. There is a definitely upward trend. So the drivers will be hedging against currency fluctuations and insecurity in the markets”.

Similar arguments have been made for gold since the world went off the gold standard, terminating its role as backing for paper currencies. But it is still used as a reserve asset by many central banks and private investors. In effect, it is much more than a commodity and has maintained monetary elements. Despite a near doubling of the gold price since the 2007 crash, many have expected much more from gold in a world of escalating financial insecurity. It could certainly be argued that it is underpriced, in part because of market short-term thinking; low consumer price inflation and high asset price inflation, and being overwhelmed by derivative trading.

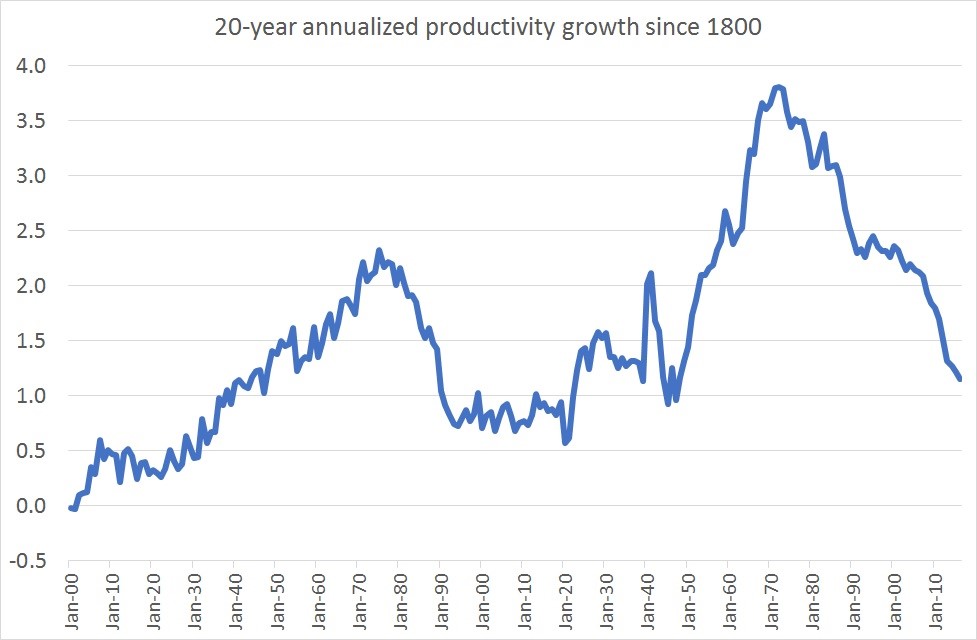

While a return to the gold standard has solicited much debate, mostly against, the value of such a disciplining instrument in monetary policy may have been vastly understated. I came across this graphic compiled by the Bank of England, and included in a report by Chris Dillow on the website evonomics.com.

A 20-year annualised view is useful in suppressing short-lived productivity gains, and highlighting longer term impact. Still, there may be some pitfalls in making too much of this. Coincidence does not necessarily equal cause and the statistics are UK specific. In his accompanying article, Dillow may have connected two distant dots in arguing that it shows that neoliberalism has failed to make people better off. But it is perhaps more than academic that the decline coincided with Milton Friedman’s influence, Reaganomics and Thatcherism, contrary to their acknowledged short-term validity.

An observation that has been made in the Keiser Report may be somewhat counter-intuitive but is far more telling and intriguing: that the decline started shortly after the gold standard had ended. That makes some sense. With gold-backed money, ill-discipline and national debt lead to a bleeding of your gold reserves. Without it you have endless money creation based on debt and declining interest rates which is not conducive to long-term investment in productive capacity, but rather encourages capital to flow to rental income, assets and capital gains. This is one explanation for the Dow hitting record highs, despite months of declining company earnings.

It is tempting for gold and cryptocurrency champions to want greater “official recognition” of these assets in monetary policies like holding Bitcoin as a reserve asset. Nothing prevents a big central bank or monetary authority from starting their own cryptocurrency or asset that can be traded publicly and rival others. That seems unlikely in the foreseeable future, and may even be counter-productive because of the inevitable controls that will be imposed on trading in them. All these assets, including gold, should simply be left to be traded freely.

Their time will come. Perhaps sooner than we may think.

TheBitcoinNews.com – Bitcoin News source since June 2011 –

Virtual currency is not legal tender, is not backed by the government, and accounts and value balances are not subject to consumer protections. TheBitcoinNews.com holds several Cryptocurrencies, and this information does NOT constitute investment advice or an offer to invest.

Everything on this website can be seen as Advertisment and most comes from Press Releases, TheBitcoinNews.com is is not responsible for any of the content of or from external sites and feeds. Sponsored posts are always flagged as this, guest posts, guest articles and PRs are most time but NOT always flagged as this. Expert opinions and Price predictions are not supported by us and comes up from 3th part websites.

Advertise with us : Advertise

Our Social Networks: Facebook Instagram Pinterest Reddit Telegram Twitter Youtube